This is how you decide whether you pay with a PIN or a signature

The bank card has long been indispensable as a means of payment. When shopping, it is increasingly replacing cash and at the checkout it says “Please enter your PIN” or “Your signature please”. But why can’t you make up your mind?

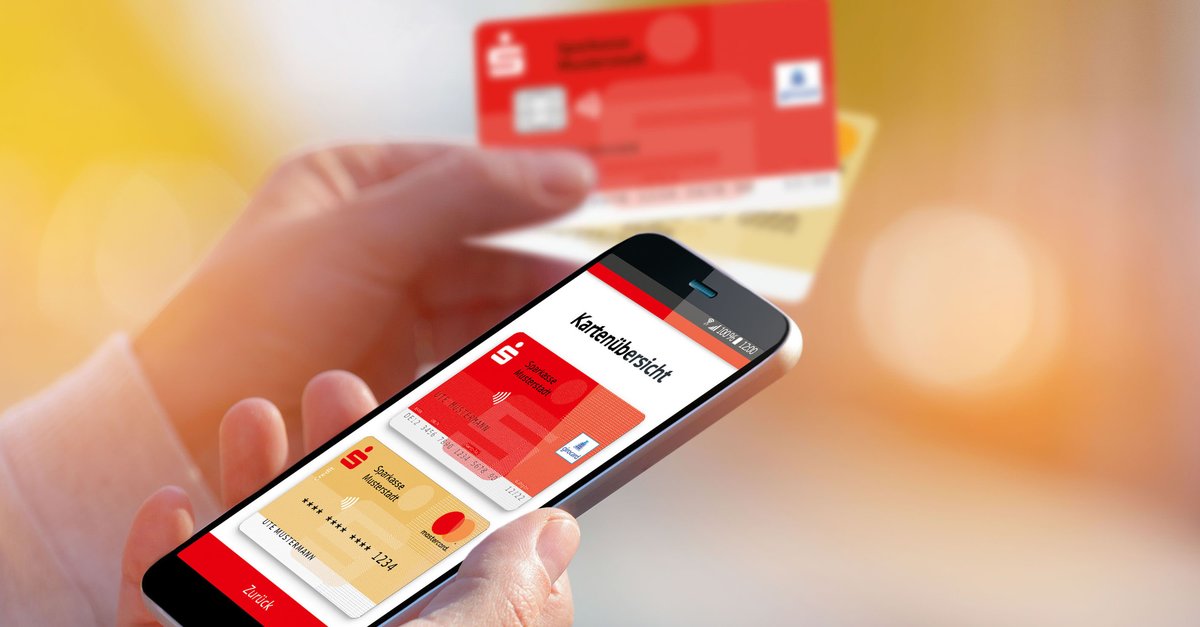

EC or giro card, ELV or PIN? You have to consider this when paying by card

Those who have not switched to mobile payment by smartphone or smartwatch anyway will often use the bank card, giro card or EC card (the old term). If you haven’t heard of one or the other, don’t worry: the different names mean one and the same thing – the card with which you access your bank account, but not the credit card.

Especially in the time of the pandemic, the giro card has become indispensable for even more customers when shopping – and since then it has finally been accepted in many more shops. but who actually decideswhether we have to enter or sign the PIN at the checkout? The short answer: the dealer and chance.

PIN or signature? Dealer makes the decision for you

If you take a closer look, the hidden process becomes a little more complicated: Because whether you are asked to enter a PIN or to sign always depends on the particular shop in which you are about to pay Traders can choose. But what is the difference?

When paying by PIN, your Account debited immediately (Source: Savings bank), the dealer receives the money and can (almost) rule out problems later. This is why it can also happen that you receive an error message at the checkout via PIN payment if you have less credit available (and no overdraft facility). However, the account balance is not communicated.

If, on the other hand, you are asked to sign, you are giving the seller permission to pay the amount at a later time by electronic direct debit (ELV) from your account. This also works if you are (too) short of cash. The problem for the retailer: Nobody knows whether you can pay or, to put it casually, buy on credit. In addition, direct debit payments are easy for you to reclaim.

If you don’t want to know anything about giro cards, you should find out more about mobile payment functions. You can see the most important things in brief in our Video:

Problem with the PIN: Signature is cheaper

For retailers, everything speaks in favor of the PIN – it is simply more secure. But the service costs: retailers usually pay around 0.2 percent of the purchase value to the relevant bank. The solution: Lots of supermarkets, retail shops or restaurants switch back and forth between the two systems. As a rule, the PIN query predominates, so there is secure income. The signature is used less often, but something can be saved here.

So if at the end of the month you run out of money, you as a customer might come up with the idea of paying with your signature and thus delaying the debiting. However, this only works if you know stores that only pay reliably by ELV.

![7 tips on how to expand your portfolio without increasing budgets [Anzeige]](https://www.basicthinking.de/blog/wp-content/uploads/2022/08/territory-header-contet-unternehmen-tipps.jpg)